Chances are you own at least a few material items that are special to you or necessary to your daily life. Most people choose to protect these items, like cars and houses, by investing in things like homeowners and car insurance.

Unfortunately, these insurance policies are not all-inclusive and there are many situations they won’t cover. For instance, if you accidentally break your neighbor’s window and they decide to sue you, you’re going to have to foot the bill on your own. This can put serious financial stress on you and your family.

The good news is there is a type of insurance policy that can help with unfortunate circumstances like this. It’s called a Personal Umbrella Policy (PUP), and it’s designed to protect you and your family against the unexpected.

What is a PUP?

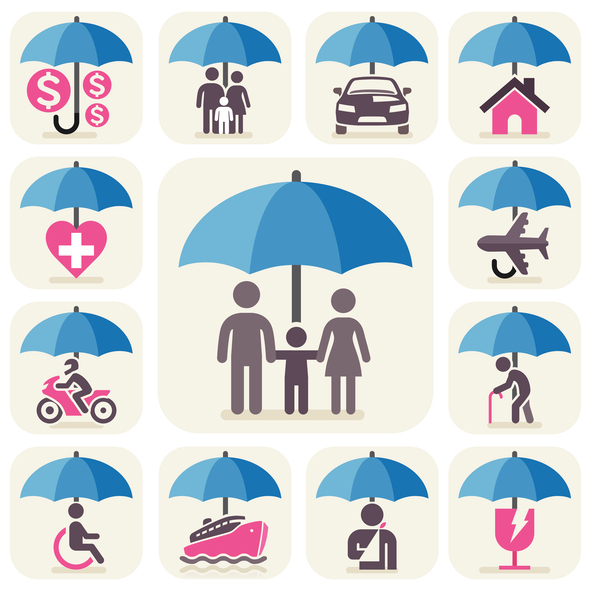

People purchase personal umbrella policies when they want to protect themselves against liability. It is an extra form of insurance that protects you and members of your household in the event you hurt someone else or damage someone else’s property. PUPs do not overlap with home, boat, or car insurance. Instead, they cover things like settlement costs or attorney’s fees after your other insurance policy limits have been exceeded.

What PUPs Cover

In addition to things like property damage and personal injury, a personal umbrella policy can also help with things like slander or false arrest. Below are some of the things that PUPs do cover that might be helpful to you:

- Personal injury to others – If you or a family member hurt someone else, that person’s medical expenses will be covered by an umbrella policy. This is true regardless of the circumstances and will include things like car accidents, attractive nuisances (in which a property owner can be held liable for injuries suffered by children if the injuries are caused by an object on the land that is likely to attract children), and other injuries that may happen on your property.

- Property damage – A pup will cover the expenses if you damage someone else’s property. This includes things like totaling someone else’s car, accidentally driving your own car into a building, or damaging school property.

- Property owners – If you are a landlord, a PUP is essential. Whether residential or commercial, a PUP will protect you if someone is injured on a property you own.

- Off-premises accidents – This coverage protects you if you hurt someone else while you aren’t on your own property. For instance, if you’re walking your dog and they bite someone, your PUP would pay for that person’s medical bills.

- Lawsuits – Umbrella policies are great protection if you are sued for things like wrongful eviction, slander, false arrest, defamation, or malicious prosecution.

What PUPs Don’t Cover

While there are a lot of scenarios that umbrella policies can help with, there are some they don’t apply to. These can include but aren’t limited to:

- Intentional damages – If you deliberately hurt someone or damage their property, your PUP isn’t going to help.

- Business losses – If you run a business, a PUP will not cover someone who is injured while doing business with you. However, you can buy a “rider,” which is specialized coverage you can add to your PUP to protect your clients.

- Exotic vehicle liability – Things like cars, golf carts, and boats are covered under a PUP, but things like planes, jet skis, or snowmobiles usually aren’t. If you are injured on an exotic vehicle you will be footing the bill whether you have a PUP or not. That said, everyone’s umbrella policy is different, so check yours to see which vehicles are covered.

- Damages to your own property – PUPs cover you if you damage someone else’s property, but they can’t help you if you damage your own. For example, if you break a window while tossing the football around, you’ll have to pay for that out of pocket unless your renter’s or homeowner’s policy covers it.

- Hired help – If you employ someone like a pool guy or landscaper, a PUP may not cover them if they are injured on your property. Occasional workers, like babysitters or house sitters, may be covered if they work less than 35 hours a week. However, if the worker is full time, you’ll need a “rider” to cover them.

Umbrella Policies and Uninsured Motorist Coverage

If you have uninsured/underinsured motorist coverage as well as a PUP policy, it’s important to talk to your insurance provider and make sure the limits align.

Your umbrella policy provides coverage where your car insurance limits end. If, for example, your umbrella policy is set to pay out when losses reach $300,001, your auto insurance should have a $300,000 cap so the coverage reaches the base of the PUP. Lower limits are often written into uninsured/underinsured motorist policies, but this can easily be adjusted with a call to your insurance agent or by tweaking your policy online if your insurance company allows web-based policy access.

Why Should I Invest in an Umbrella Policy?

You can handle a situation where you injure someone or damage their property on your own. It will be expensive, but it is possible. That said, it’s much easier and safer to expect the unexpected and purchase a personal umbrella policy to help with these scenarios.

If you still aren’t sure if a PUP is right for you and your family, here are some additional reasons you may want one:

- It gives you peace of mind. Having a PUP can take some of the worry and “what ifs” out of your life.

- We live in a sue happy world. If you hurt someone else or damage their property, they may take that as an opportunity to get as much money out of you as possible through a lawsuit.

- PUPs are cheap. With most insurance companies, you can get $1 million worth of coverage for as little as $15 a month.

- It’s worth it for the price. It’s like having a life insurance policy or paying for disability insurance at your job. You may never need to use it, but if you do, you’ll be glad you have it.

When deciding whether or not to purchase an umbrella policy, remember this: most people only carry the minimum insurance coverage required by law. Some people, unfortunately, don’t carry any insurance at all.

If you’re injured by someone who doesn’t have a PUP, and your own insurance limits run out, you could be left with massive bills for your medical expenses and damages. At Hauptman, O’Brien, Wolf & Lathrop, P.C., our job is to make sure you receive the compensation you’re entitled to. No matter what happened, if you’ve been hurt by someone else’s negligence our experienced Omaha personal injury attorneys are here to look out for your best interests. Contact us to schedule your free consultation or call us at (402) 241-5020.